3 Graphs Showing Why Today’s Housing Market Isn’t Like 2008

3 Graphs Showing Why Today’s Housing Market Isn’t Like 2008 With all the headlines and talk in the media about the shift in the housing market, you might be thinking this is a housing bubble. It’s only natural for those thoughts to creep in that make you think it could be a repeat of what took pla

Read More

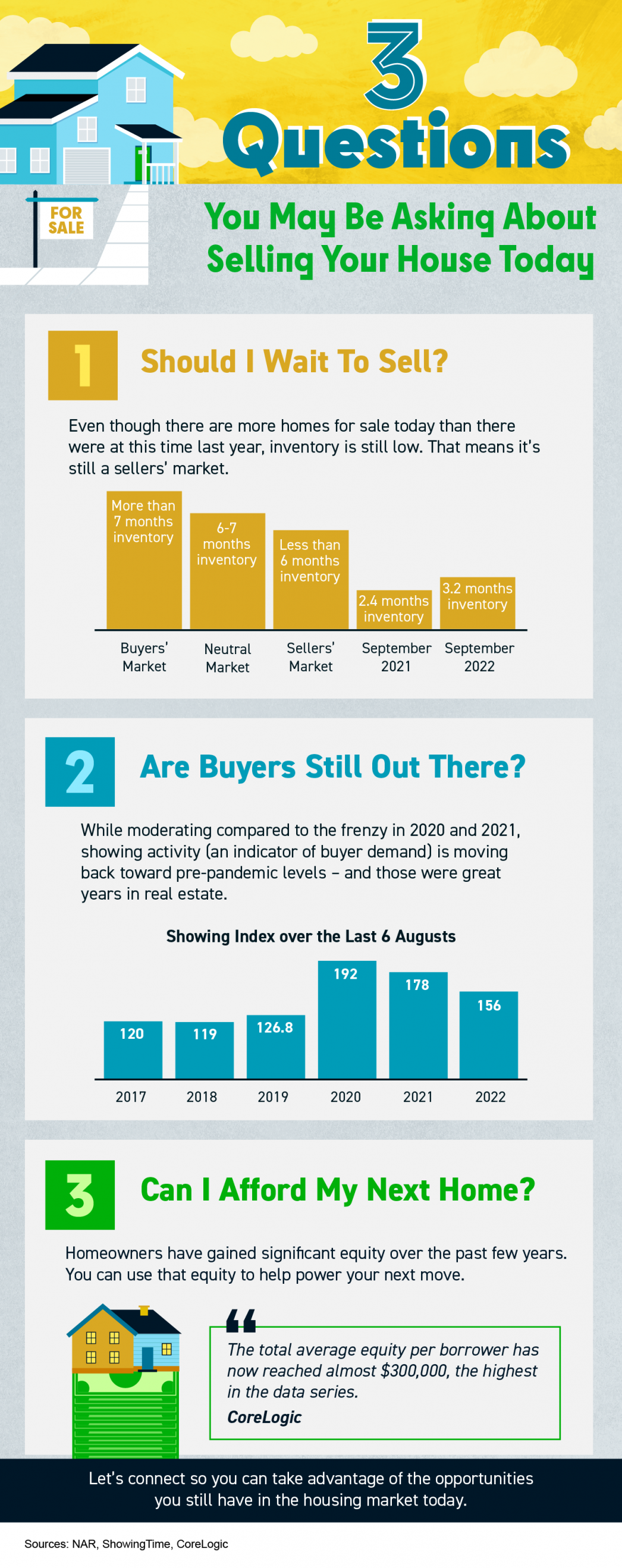

3 Questions You May Be Asking About Selling Your House Today

3 Questions You May Be Asking About Selling Your House Today [INFOGRAPHIC] Some Highlights If you’re planning to sell your house this year, you likely have questions about what the shift in the housing market means for your home sale. You might be wondering: Should I wait to sell? Are buyers stil

Read More

Four Things That Help Determine Your Mortgage Rate

Four Things That Help Determine Your Mortgage Rate If you’re looking to buy a home, you probably want to secure the lowest interest rate possible for your home loan. Over the last couple of years, that was easier to do as the housing market saw record-low mortgage rates, but this year rates have r

Read More

What Are Experts Saying About the Fall Housing Market?

What Are Experts Saying About the Fall Housing Market? The housing market is rapidly changing from the peak frenzy it saw over the past two years. That means you probably have questions about what your best move is if you’re thinking of buying or selling this fall. To help you make a confident dec

Read More

Categories

Recent Posts